Scheduled Income Tax Cuts to Mostly Benefit High-Income Households

Individual Income Tax Rate Set to Fall from 3.99% to 3.49% in 2027 and 2.99% in 2028

The latest Consensus Revenue Forecast, issued on May 15, 2026, projects General Fund net tax collections will exceed income tax cut triggers in FY 2025-26 and FY 2026-27. This means the individual income tax rate will automatically decrease, by statute, from 3.99% to 3.49% beginning in tax year 2027, and from 3.49% to 2.99% in 2028. The consensus revenue forecast for both fiscal years is more than $1 billion higher than the level necessary to trigger these rate reductions, which will reduce revenue by approximately $5 billion by FY 2028-29 compared to holding the rate at 3.99%. Under OSBM’s May 2026 long-run revenue projections, revenue collections in FY 2032-33 would be above that year’s statutory trigger and result in a further rate cut to 2.49% in 2034.

Compared to current-law projections, the North Carolina General Assembly (NCGA) leadership’s proposed tax cut plan would lower individual income rates more gradually:

- 2027-2029 – 0.5% rate reduction to 3.49%

- 2030-2032 – 0.25% rate reduction to 3.24%

- 2033-2034 – 0.25% rate reduction to 2.99%

- 2035 and after – potential for two quarter-point rate reductions to 2.49% subject to revenue triggers

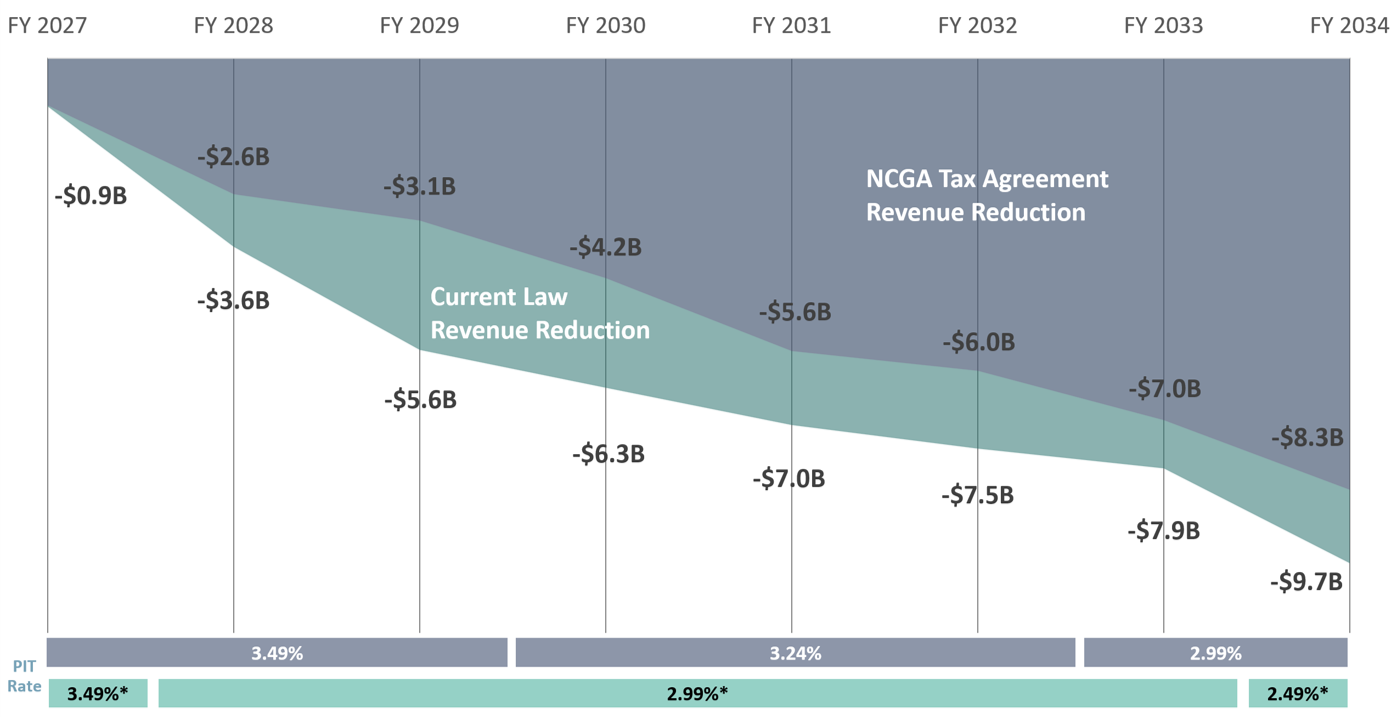

The chart below shows the size of rate reductions under current law projections and NCGA leadership’s proposed tax plan.

Smaller Revenue Reductions Under NCGA Agreement Compared to Current Law

Revenue in billions compared to 2026 policy (i.e. 3.99% individual income tax rate and 2% corporate income tax rate)

Fiscal Impacts of Individual and Corporate Income Tax Rate Cuts

- The individual and corporate income tax rate cuts will reduce General Fund revenues by approximately $0.9 billion in FY 2026-27. That loss grows to $9.7 billion by FY 2033-34. Due to back-to-back 0.5% reductions in the individual income tax rate in 2027 and 2028, the annual revenue loss rises by more than 50% between FY 2027-28 and FY 2028-29.

- The tax cut plan proposed by NCGA leadership decreases individual income tax rates more gradually but maintains the same scheduled phaseout of the corporate income tax in 2030. By FY 2033-34, the individual income tax rate cuts under the proposal will still reduce revenues by an estimated $6.5 billion plus an additional $1.8 billion revenue loss from phasing out the corporate income tax.

- Cumulative General Fund revenue losses over the next eight years (FY 2026-27 through FY 2032-34) total more than $48 billion under current law and more than $37 billion under the NCGA leadership plan based on OSBM’s estimates. That’s more than the entire $32 billion budget for FY 2025-26.

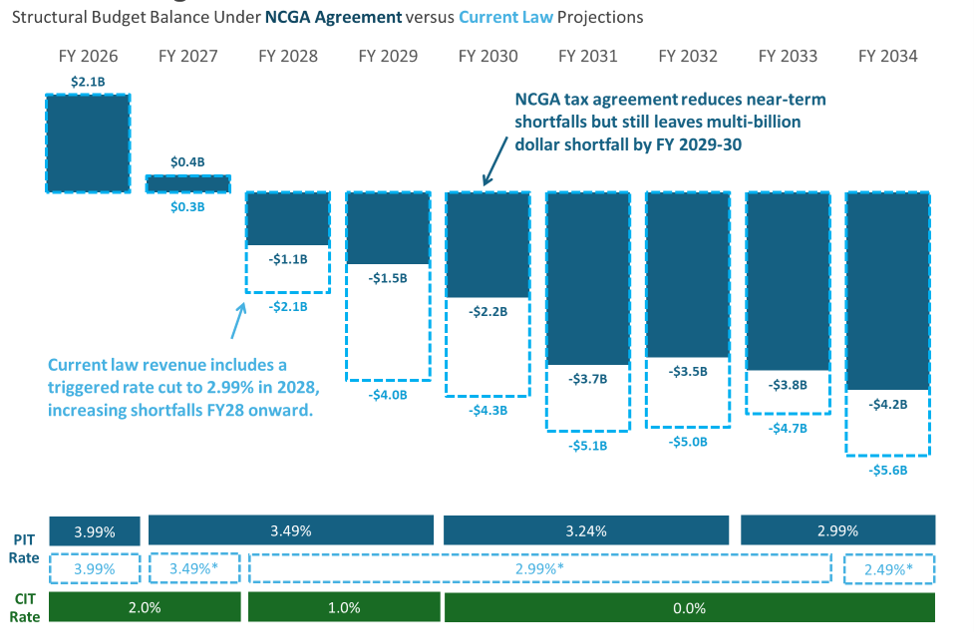

Income Tax Cuts Would Lead to a Large Structural Shortfall

The chart below shows the projected structural budget balance under a current-services baseline using the enacted FY 2025-26 budget, plus $319M in supplemental appropriations for Medicaid, and growing by projected population growth and inflation as measured by the price index for state and local government expenditures. NCGA leadership’s proposed tax rate schedule would reduce the size of shortfalls in future years but will still lead to multi-billion-dollar shortfalls beginning in FY 2029-30.

Chart: Individual and Corporate Income Tax Cuts to Reduce Annual Revenues by $7 Billion in FY 2031-32

Note: Tax rates listed are those in effect as of January 1st in each fiscal year.

* The consensus revenue forecast projects hitting the first personal income tax rate cut trigger in FY26 and the second in FY27. OSBM forecasts hitting the third trigger in FY33.

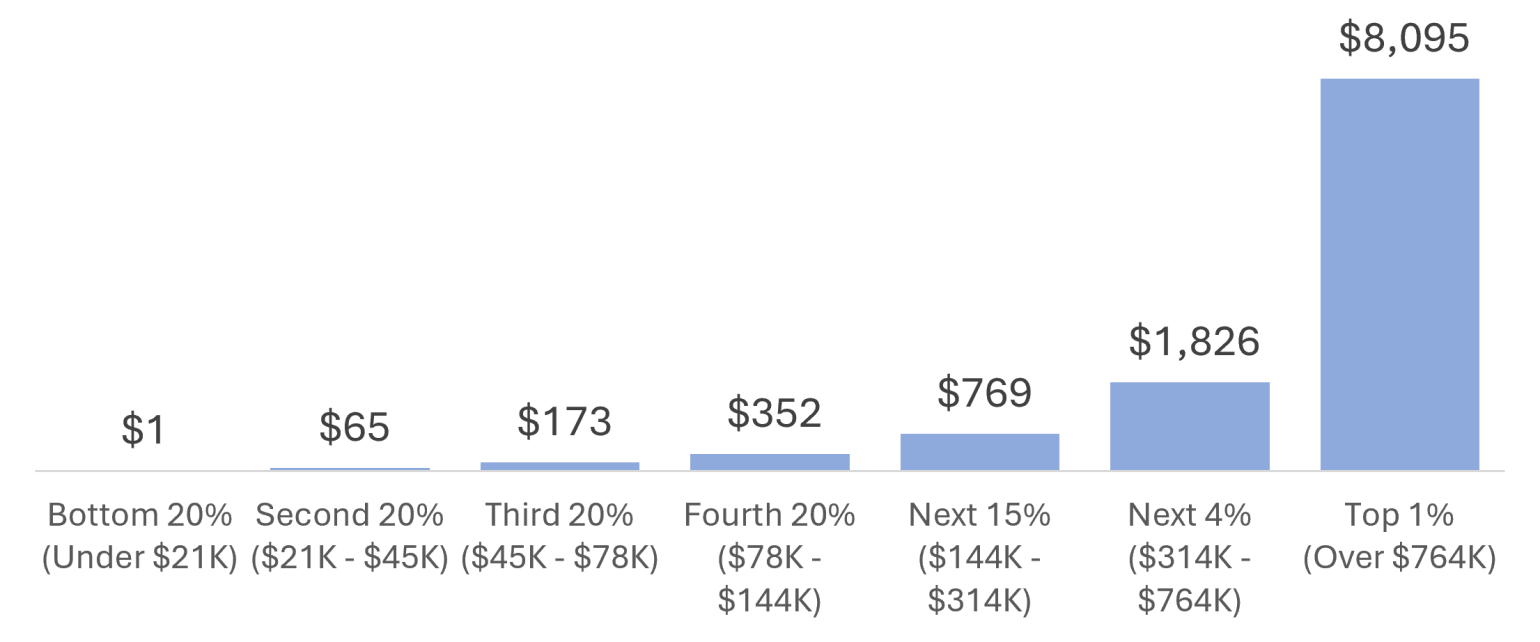

High-Income Households to Benefit Most from Income Tax Cuts

The chart below shows the estimated tax savings from the anticipated cut in the individual income tax rate from 3.99% to 3.49% in 2027, by income level, among North Carolina residents who file a state income tax return.

Chart: Size of Tax Cut by Income Group (NC Resident TY 2027)

Key Distributional Impacts of Tax Rate Cut

- The tax cut disproportionately benefits higher-income taxpayers. Households in the top 1% by income will see an average tax reduction of over $8,000, while the majority of NC households will receive a tax cut of less than $170.

- Approximately 38% of North Carolina households who file a state tax return will receive a tax reduction of less than $100. Roughly 1 million of these households have no taxable income after subtracting deductions and will receive no benefit from the tax rate cut. Nearly all of these households have incomes under $40,000.

- An estimated 1.5 million North Carolinians who live in households that have incomes too low to file a state tax return—and who are not represented in the analysis above—will not benefit from the individual income tax rate reduction.

- The top 5% of taxpayers by income will receive more than 40% of the total tax cut for full-year state residents ($742 million), while the bottom 40% of households filing a state tax return will share just 3.3% ($60 million).1

- Over 6% of the total tax cut (about $120 million) will benefit residents of other states who earn income in North Carolina but do not live here. Among nonresidents, those with the highest incomes benefit disproportionately: the top 1% of non-resident filers—those with incomes of more than $18 million—will receive an average tax savings of $9,500, totaling $46 million.

- This lower tax rate will reduce state revenues by approximately $2.3 billion in FY 2027-28. This amount is comparable to the entire budget for the Division of Adult Correction and exceeds the annual appropriation for community colleges. The revenues not collected due to the tax cuts are funds that could otherwise support services benefiting all North Carolinians.

- 1

The percentages of the tax cut are based on the share attributed to households filing a D-400 tax return, which accounts for most of the impact of the income tax cut. Roughly 10% of the impact is attributed to part-time and non-residents. An additional 10% of the impact of the tax cut is attributable to non-household entities (such as estates and trusts) and other payments not accounted for in tax return filings.